HOW TO DISSOLVE A COMPANY?

A company is legally dissolved after it files a final tax return, and pays any outstanding taxes. A business cannot legally operate once it has been dissolved. Any contracts the company entered into during or after its existence as a legal entity are still valid and enforceable, provided the other party consents to dealing with the ‘former’ company.

The shareholders of a company have three options when they want to shut down a business: They can sell the assets of the company and distribute the proceeds among themselves; they can continue with a limited liability partnership (LLP); or they can put in place an orderly winding up procedure through which creditors will be paid from available funds.

What does company dissolution mean?

A company can be dissolved voluntarily by its shareholders or involuntarily through a court order of dissolution. A company is said to be ‘voluntarily’ dissolved when the following steps are taken:

The board passes a special resolution stating that it will no longer carry on business and authorizes the appointed liquidator, if any, to complete the process of dissolution. The appointed liquidator then makes all necessary formalities, such as giving notice of his appointment, publishing advertisements in newspapers regarding the winding up proceedings and calling a meeting of creditors for receiving their sanction for dissolving the company.

After these formalities have been completed with the consent of all members and creditors, if any, he files an application with the Registrar seeking registration as a dissolved company. The company is then dissolved in the hands of the registered agent, who issues a certificate of dissolution to that effect after making all necessary entries in the register.

A company can be ‘involuntarily’ dissolved either by operation of law or by the Court on application by any aggrieved person. For instance, when a company fails to file its financial statements within statutory limits for three successive accounting years, it may be automatically dissolved by the Registrar under section 248(1) of Companies Act 1956 (the present Companies Act, 2013 contains similar provisions). Similarly, if a company fails to file its annual return for two consecutive years along with an additional fee prescribed for late filing under section 204C of Companies Act 1957 , it will also be automatically deemed to be dissolved by the Registrar under section 248(2) of the present Act. Same is the fate of a company if it does not commence its business within one year from the date shown in the certificate of incorporation or carries on business for three years without getting itself registered under section 12AA of Income Tax Act 1961. In such cases, its name will be struck off from the register and a notice issued to that effect by the ROC.

The shareholders can also apply to court for dissolution of a company if they are unable to resolve disputes among themselves regarding control over management of affairs. The Court may order dissolution if any member has been persistently making a demand that his consent as a member is necessary but continues to remain outvoted by others, or if there has been any deadlock in the company’s affairs.

Is it the same as liquidation?

No, liquidation is entirely different from dissolution. The term liquidation is generally used in the context of winding up, whereby a company voluntarily ceases its business activities and ensures that all debts are duly paid. However, it may also refer to winding up under compulsory orders by the Court, meaning the compulsory dismantling of a company’s assets for their realization and distribution among its creditors or members, while dissolution on the other hand is the winding up of a company’s affairs through its own efforts.

Liquidation is an official, supervised process by which a company’s existence is brought to an end in strict accordance with the appropriate laws and regulations, while dissolution is a more informal resolution of disputes among members or creditors regarding company affairs. When shareholders decide to wind up their business voluntarily, they may opt for dissolution instead of liquidation if they are unable to negotiate their differences amicably. However, winding-up proceedings are usually preceded by dissolution because it ensures that judicial intervention in case of any deadlock does not become necessary at all.

What are the consequences of my company being dissolved?

The consequences for your company depend upon whether you had applied for voluntary dissolution or were dissolved by the Registrar on account of statutory provisions. In most cases, voluntary dissolution without liquidation is less harmful than compulsory liquidation with winding up.

For instance, if your company was dissolved voluntarily and you later wish to continue its activities again, it is always possible to re-register the concern as a new company and commence business afresh. You will not be required to pay any penalty or fee for dissolution and re-registration under section 560(1)(d) of Companies Act 2013 (no such provision has been made in the present Companies Act, 1956; however, you may now need not pay any fee for dissolution as well as re-registration). Your shareholders or members will also retain their original rights as before. However, if your company was wound up under the Court’s supervision, it will not be possible for you to re-register or commence business afresh.

What do I have to do before closing down my company?

These are what you need to do before closing down your company:

1. Make necessary arrangements for the distribution of company’s assets among its shareholders and creditors.

2. Update your records and accounts in order to ensure that they are kept updated till the last day of operations.

3. Ensure that all debts owed by your company are duly paid off before filing documents at the ROC for closure of operations.

4. Keep an accurate record of all major events such as changes in shareholding, appointment/termination of directors, key managerial personnel and employees, etc., and file these reports with the Registrar (if required).

5. If you wish to re-register your company in future: file application along with fee prescribed under section 560(1)(d)of Companies Act 2013 for dissolution with a restitution certificate from a civil court.

6. File all documents at the ROC without delay after closure of company’s operations, and obtain a “Certificate of Closure” from the Registrar. This is important because if you fail to do so within the statutory time limit, your creditors or members may initiate winding-up proceedings against you under section 560A of Companies Act 2013 (no such provision has been made in Companies Act 1956). In such circumstances, it will be extremely difficult for you to defend yourself from their legal action.

7. If your articles of association provide for any specific period after which no member can withdraw his shares on account of non-payment of nominal share capital: send a notice to each shareholder informing him that you are about to close down the company, and that unless he pays up his share capital within a specified period of 30 days or your notice, whichever is earlier, you will proceed with winding up the company completely.

8. Ensure that all statutory provisions are complied with before filing documents at the ROC for closure of operations.

9. If there is any property belonging to your company which is still in its “C” form (unsold), obtain separate receipts from every purchaser along with acknowledgement of payment by each disinterested director/member as per section 157(2)of Companies Act 2013 if you decide not to register these transfers because articles do not allow transferability of shares/interests.

You should also make necessary arrangements for the distribution of company assets among its shareholders and creditors, if any. If you wish to re-register your company in future, file application along with a fee prescribed under section 560(1)(d) of Companies Act 2013 for dissolution with a restitution certificate from a civil court after obtaining a “Certificate of Closure” from the Registrar.

You have to ensure compliance with all statutory provisions before filing documents at the ROC for closure of operations. Keep an accurate record of all major events such as changes in shareholding, appointment/termination of directors, key managerial personnel and employees, etc., and file these reports with the Registrar (if required).

Need further help?

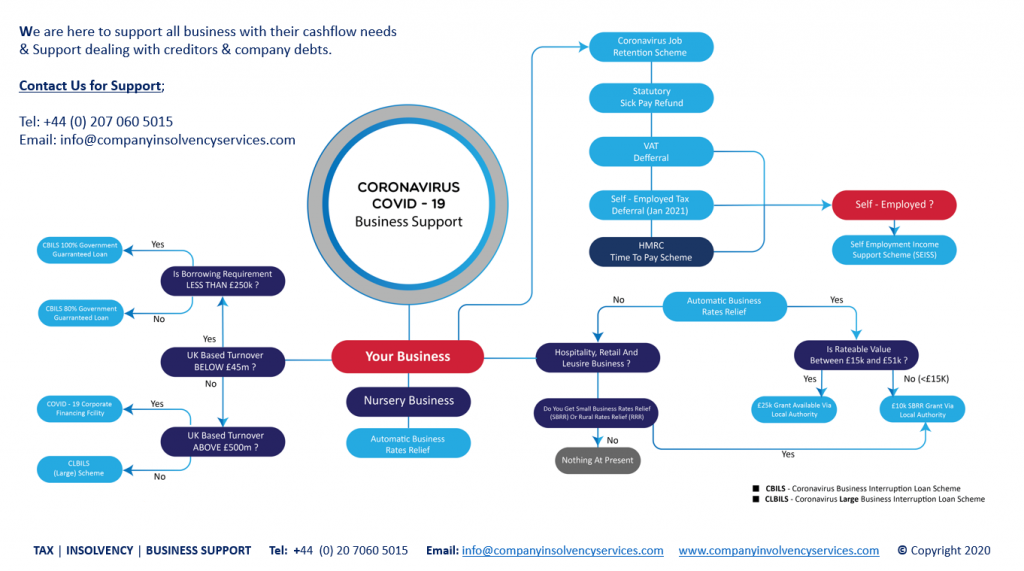

If you are unsure how this process works, or if you have any concerns about what your company’s future is likely to be, don’t hesitate to get in touch with the team today on +44 (0) 20 7060 5015 or email us @info@companyinsolvencyservices.com